Agentic Commerce Compliance: Why the Boring Layer Is the One That Unlocks the Money

Everyone is racing to let AI agents check out. The winners will be whoever can prove what an agent bought, why, and on whose authority. A practitioner's guide to agentic commerce compliance, why it is the growth layer and not the friction, and the controls every autonomous transaction needs.

Here is a prediction I will happily be held to. The companies that win agentic commerce will not be the ones that let an AI agent check out the fastest. They will be the ones that can prove, six months later, exactly what their agent bought, why, and on whose authority.

That sounds backwards, so let me say it plainly. In the agent economy, compliance is not the brake. It is the engine.

Everyone is sprinting in the other direction right now, and you can understand why, because the plumbing is finally here. Stripe and OpenAI shipped the Agentic Commerce Protocol. Google shipped the Agent Payments Protocol, AP2. Coinbase has x402. An agent can now discover a service, agree a price, and pay for it in a single exchange with no human anywhere near the transaction. The checkout problem is, for practical purposes, solved.

Which means the checkout problem was never the hard one. The hard one is the question everybody is speed-walking past: when software spends money on its own, who is accountable, and how do you prove it? That question has a name. It is agentic commerce compliance, and it is about to be the most valuable boring thing in the industry.

A note before we go further: this is a practitioner's guide for teams building with agents, not legal advice. I am going to talk about controls and architecture, not your specific regulatory obligations. For those, talk to actual counsel.

What is agentic commerce compliance, in plain terms

Strip the corporate vocabulary off it and agentic commerce compliance is just the ability to answer four questions about any purchase an agent makes:

- Who authorized this agent to act?

- What was it allowed to do, and did it stay inside those limits?

- Can you prove both of the above after the fact?

- When it goes wrong, who is responsible?

A human buyer answers all four automatically, just by being a human who clicked a button. They consented, their card had a limit, the receipt is the proof, and they are the accountable party. The entire apparatus of commerce compliance was quietly built on the assumption that a person is standing at the checkout. Remove the person and the apparatus has nothing to grip.

That is the whole problem in one sentence. And it is why agentic ai compliance is not the same document as your existing compliance policy with the word "agent" pasted in.

Agentic commerce versus traditional e-commerce: where the old model snaps

Put the two side by side and the fracture line is obvious.

In traditional e-commerce, intent and identity arrive together. The same human who wants the thing is the one who pays for it and the one you can call when the charge is disputed. Consent is contemporaneous. It happens at the moment of purchase.

In agentic commerce, intent and action come apart. A person delegates a goal to an agent on Monday, "keep my cloud costs under control," and the agent makes a purchase on Thursday that the person never specifically saw. The consent was real, but it was general and it was in the past. Agentic checkout does not remove the human's consent. It time-shifts it, and time-shifted consent is exactly the thing audit trails exist to reconstruct.

This is also why agentic commerce fraud prevention is a genuinely new discipline rather than a reskin of card fraud. The old signals, this device, this location, this spending pattern for this human, degrade when the buyer is software that can spin up, act, and disappear. Agentic ai in fraud prevention has to lean on what the agent can prove about itself, not on behavioral fingerprints of a person who was never there. No verifiable identity, no fraud model worth the name.

The protocols solved the plumbing, not the policy

I want to be precise and fair here, because the protocol teams did excellent work. ACP, AP2, and x402 are real infrastructure and they matter.

They are also, every one of them, answers to the question "how does an agent pay?" None of them is an answer to "what is this agent allowed to buy, and who has to sign off when it spends more than it should?" A payment rail moves money. It does not have an opinion about whether the money should have moved. That opinion, encoded and enforced, is policy, and policy is the layer that turns a transaction from possible into permitted.

You can see the market discovering this gap in real time. Security teams are already publishing frameworks for the safe use of these protocols. Buyers are already searching for vendors and tools that offer agentic commerce protection. The plumbing shipped, the water is flowing, and now everyone is looking around for the valves. The valves are compliance.

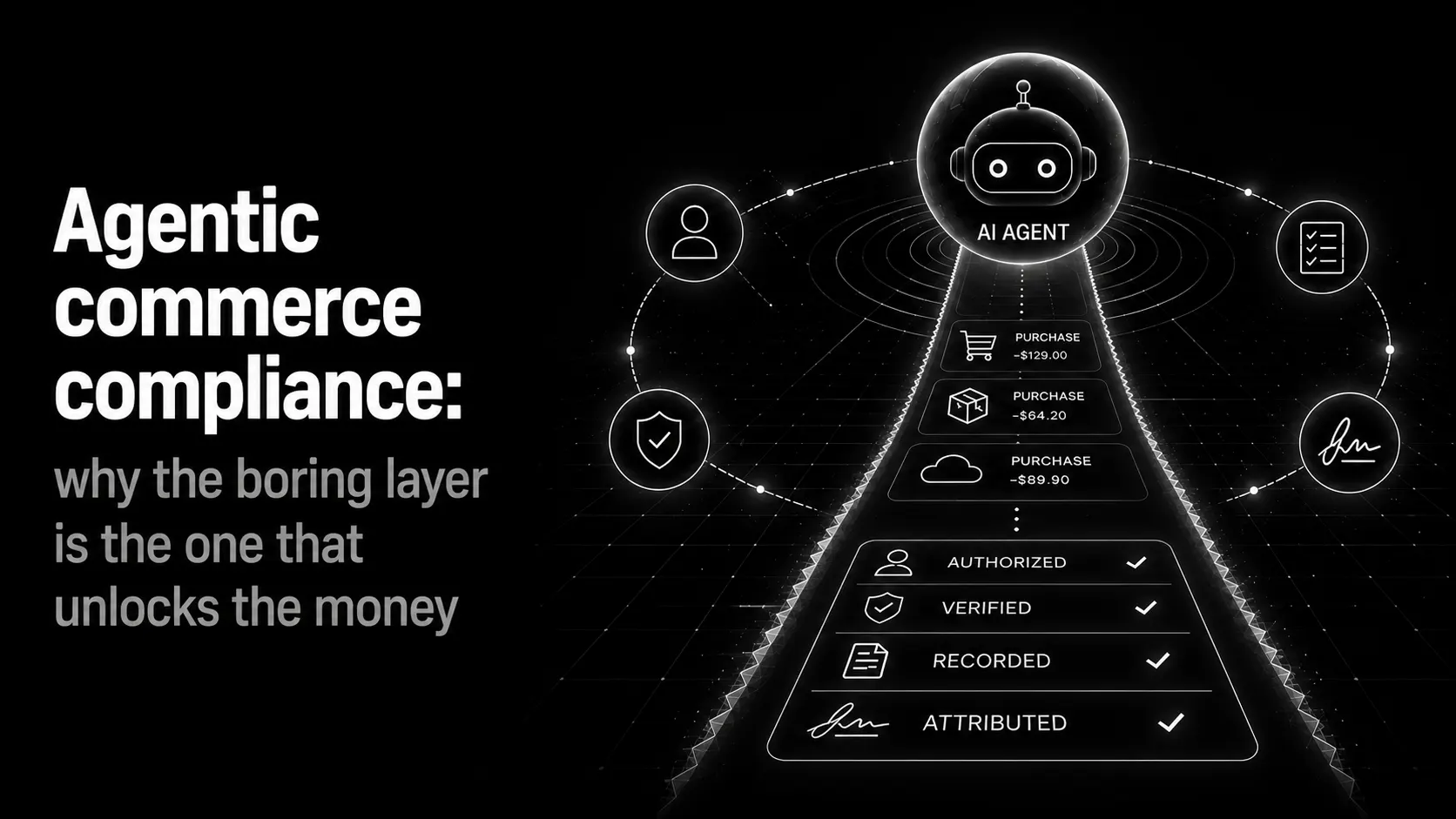

The four controls every compliant agentic transaction needs

If you are doing agentic commerce era business preparation and you want something more useful than anxiety, here is the practical core. Four controls, vendor-neutral, in the order that matters.

- Identity. Every agent and the party it acts for must be nameable and verifiable. This is the foundation, and it is the same idea I argued in Know Your Agent: an anonymous agent with a budget is a liability with no name attached. Agentic ai for kyc and compliance starts here, because you cannot govern what you cannot identify.

- Policy. Spend limits, allowlists, category restrictions, and approval thresholds, enforced before a transaction executes rather than reviewed after. A rule that lives in a prompt is a suggestion. A rule enforced at the signing layer is a control. Only one of those survives an audit.

- Audit. An immutable record of what the agent did and the reason it did it. Not a log you hope is complete, but a trail you can hand to a finance team or a regulator and have it hold up.

- Attribution. A clean line from every action back to an accountable human or entity. When the question "who is responsible for this purchase?" comes, attribution is the difference between a one-line answer and a forensic investigation.

Identity, policy, audit, attribution. Notice that none of these is about making the agent more capable. Every one is about making it more accountable, and accountability is the precondition for trust, which is the precondition for budget.

Why compliance is the growth layer, not the friction

Now the contrarian part, stated as plainly as I can.

No enterprise is going to hand an autonomous agent a meaningful budget until it can govern and audit that agent. None. The CFO who would be fired for letting an employee spend without limits or records is not going to extend that trust to software just because the demo was slick. The thing standing between agentic commerce and real money is not better models or faster checkout. It is the ability to deploy an agent and still sleep at night.

Which means the compliance layer is not the tax you pay to do agentic commerce. It is the key that unlocks the spend. The first platforms to make agent governance boring, provable, and built-in will be the ones enterprises actually route their budgets through. Commercial use cases for programmable agentic payments do not scale on capability. They scale on control.

This is the part the speed-runners have backwards. They are optimizing for the agent that can buy the most things. The market will reward the agent you can trust with the most money. Those are very different optimization targets, and only one of them has a CFO's signature on it.

Where this is heading

The honest state of things: the rails are live, the controls are not standardized, and most teams shipping agents today are doing agentic checkout with governance held together by hope and a spreadsheet. That gap closes one of two ways. Either every team rebuilds identity, policy, audit, and attribution from scratch, badly, in isolation, or the controls become infrastructure you plug into, the same way the payment rails did.

This is the layer we are building toward at Abstraxn. Identity through ERC-8004, programmable wallets, and multi-rail payments are live today. Programmable policy at the signing layer, the enforce-before-execution control this whole piece is about, is in active development, precisely because it is the part the market has not yet solved. I am not going to pretend it ships tomorrow. I am going to tell you it is the right problem, and that the teams treating compliance as the growth layer are the ones who will still be standing when the budgets show up.

So here is the question I will leave you with, and I genuinely want the argument: is agentic commerce compliance a cost center that slows your agents down, or the single thing that will decide which agent economy platforms enterprises actually trust with real money? I know where I land. Tell me where you do.

Key Takeaways

- Agentic commerce compliance is the ability to answer four questions about any agent purchase: who authorized it, within what limits, how it can be proven, and who is accountable. It is governance, not plumbing.

- The old compliance model assumes a human at the checkout. Agentic commerce versus traditional e-commerce breaks on time-shifted consent: the human delegates a goal in advance, the agent acts later, and audit trails exist to reconstruct that gap.

- ACP, AP2, and x402 standardize how agents pay. None of them decides what an agent may buy or produces an audit trail, so compliance is the layer built on top of the rails.

- The four controls every compliant agentic transaction needs are identity, policy, audit, and attribution. None makes the agent more capable; all make it more accountable.

- Compliance is the growth layer. Enterprises will not extend real budgets to agents they cannot govern, so the platforms that make agent governance built-in are the ones that unlock the spend.

Frequently Asked Questions

What is agentic commerce compliance? It is the set of controls, attribution, and audit that make a purchase initiated by an autonomous AI agent accountable. It answers four questions for every transaction: who authorized the agent, within what limits it was allowed to act, how that can be proven after the fact, and who is responsible when something goes wrong. It is the governance layer on top of payment protocols like ACP, AP2, and x402, which standardize how an agent pays but not what it is permitted to buy.

How is agentic commerce different from traditional e-commerce? In traditional e-commerce a human clicks buy, which creates clear intent, consent, and a person to hold accountable. In agentic commerce the human is removed from the moment of purchase, so consent is delegated in advance and accountability has to be reconstructed from records. That shift is why the old compliance model does not transfer cleanly and why agentic checkout needs its own controls.

Do ACP, AP2, and x402 handle compliance? Not on their own. The Agentic Commerce Protocol from Stripe and OpenAI, Google's Agent Payments Protocol (AP2), and Coinbase's x402 standardize how an agent discovers a service and pays for it. They do not decide what an agent is allowed to spend, enforce limits at signing, or produce the audit trail a finance or risk team needs. Compliance is built on top of the rails, not inside them.

What controls does an autonomous payment agent need to be compliant? At minimum: a verifiable identity so the agent and its principal can be named, programmable policy that enforces spend limits and allowlists before a transaction executes, an immutable audit trail that records what happened and why, and clear attribution that ties every action back to an accountable party. Identity plus policy plus audit plus attribution is the practical core of agentic AI compliance.

Is this legal or regulatory advice? No. This is an operational guide for teams building and deploying autonomous agents. It describes the controls and architecture that make agent transactions auditable and governable. It is not legal, compliance, or regulatory advice, and you should consult qualified counsel for obligations specific to your jurisdiction and industry.

About the Author

Parth Chaudhary

Solution Architect

Parth Chaudhary is a Solution Architect at Antier, the team behind Abstraxn. He currently works at the intersection of account abstraction and agentic AI infrastructure, consistently shipping wallets, paymasters, identity primitives, and policy guardrails for autonomous agents in production. Find out more at abstraxn.com or easily spin up an agent at dashboard.abstraxn.com.